The Baseline

Step 1 – Determine Your current budget

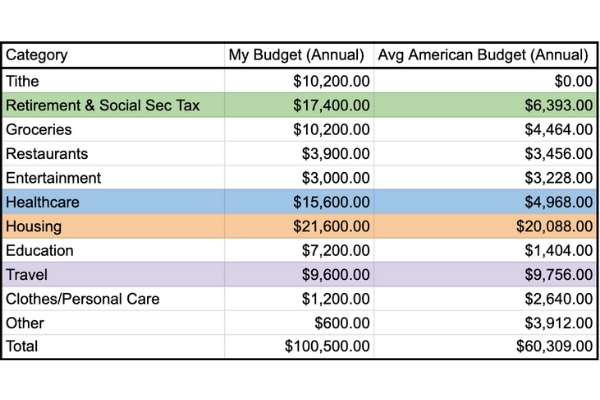

How much does your current lifestyle cost? If you don’t know, start tracking everything you spend. You need to get a baseline of your expenses. I used to track my expenses with mint. Now I live in a place where credit and debit cards aren’t used, so I track all my expenses with google sheets and google forms. Here’s what my budget looks like:

I need $100,500 a year to maintain my current lifestyle and I’m currently saving $9,000.00 a year towards FI. Note how much you’re saving towards retirement, you’ll need that figure later. Here’s how my budget compares to the average American’s budget (as of 2018). I combined the like-colored rows from my budget to make it easier to compare the two.

This average American’s budget budget is based on an average of 2.5 people per “consumer unit”. At first I was kinda discouraged, because our budget is way higher than average, but we have 5 people in our family, so that explains part of the difference. We also give more, save more and insure more than average.

Post FI Projections

Step 3 – Project Future Budget

Now that we’ve got our baseline, it’s time to look forward. In order to calculate how much we need for FI we really need to know what our budget will be post-FI. So, we need to spend some time thinking about how our budget might change post-FI.

This goes back to knowing your “why”. For example, if you want to travel 24/7 you’ll increase your travel budget. If you want to stay right where you are and do volunteer or ministry work, your post-FI budget might look pretty similar. Some good questions to ask are:

- Will you live in the same house/apartment?

- Will you want to travel more?

- Will you want to go back to school?

- Will you have (or still have) kids living with you? This will hugely impact categories like education, groceries, entertainment.

- Will you continue to need to save for anything….seems kinda obvious but don’t forget to zero out the retirement savings line if you no longer need to save.

- Will your level of giving change?

- Will your healthcare related costs change? We know health costs just go up as we age. Also, if you’re planning to FI and leave employer-provided healthcare, this is a big one.

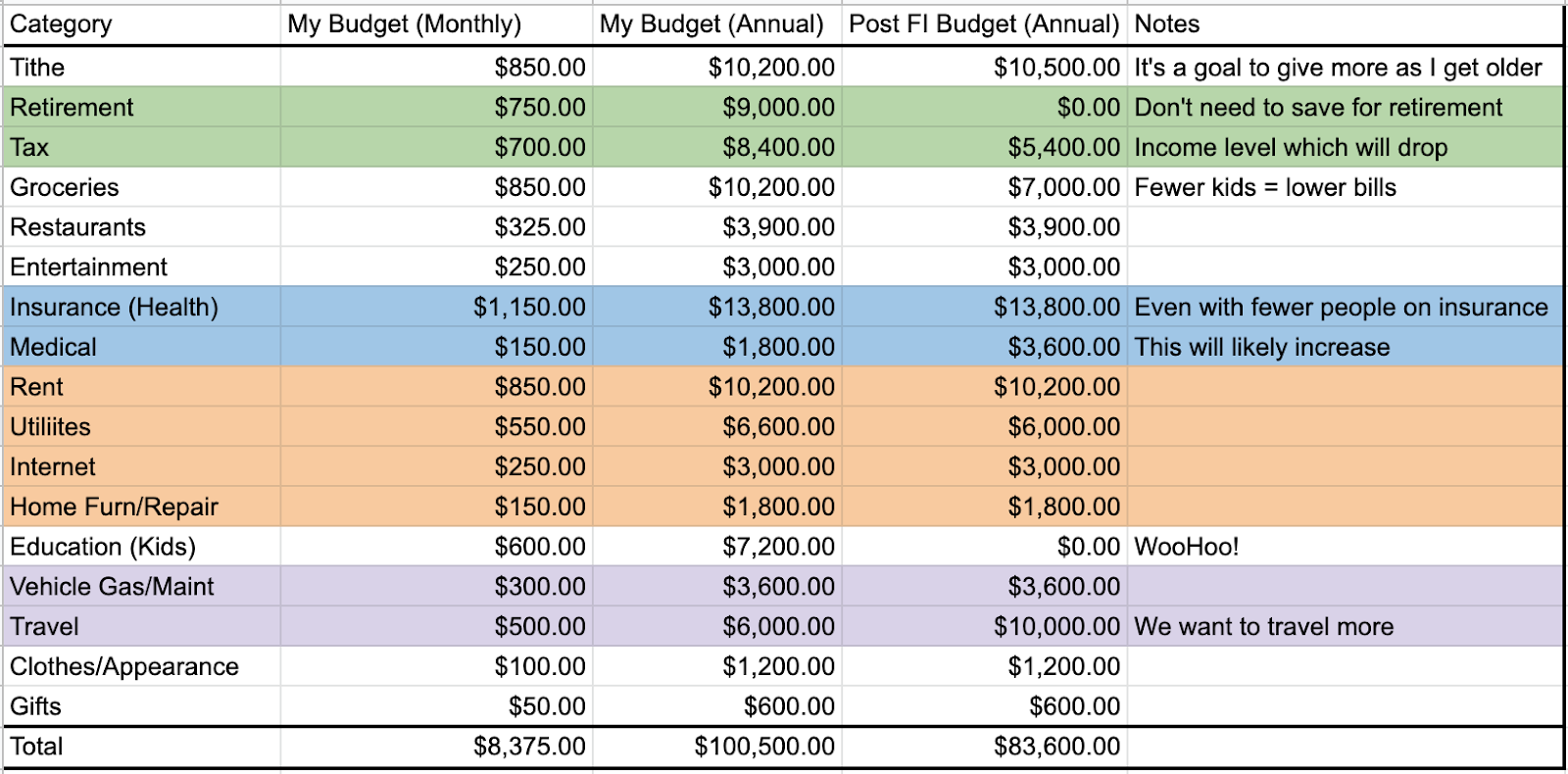

Here’s my update budget with some notes so you can see my thought process.

I project I’ll need $83,600.00 a year post-FI. I probably could have lowered the budget even further but I want to err on the conservative side.

Step 6 – Choose SWR

Now, it’s time to select our withdrawal rate. Withdraw rate means what percentage of our FI investments we’re going to withdraw each year. Based on the Trinity Study, we can withdraw 4% a year and be relatively certain that it will last at least 30 years.

People on the more conservative end (yours truly) or those that are looking to FI earlier in life and need their savings to last upwards of 50 years may choose a lower withdrawal rate, such as 3.5%. This killer article from thepoorswiss.com walks through all the details and shows that with our example asset allocation and a 3.5% withdrawal rate, we have a 98% chance of not running out of money, even after 50 years!